You approve a plan that assumes “average” revenue growth, “average” volatility, and an “average” customer. Then reality shows up: a cluster of bad quarters, a tail‑risk event, a segment that behaves nothing like the model. The problem wasn’t bad luck; it was the flaw of averages — the comforting but dangerous belief that things will naturally “even out” over time.

When you manage money or run a business, trusting that “things will even out” is not a risk-management strategy; it’s a cognitive trap.

This piece is about why the “law of averages” quietly sabotages gamblers, investors, and leaders, and how to design decisions that work in the real world of streaks, outliers, and fat tails.

Our brains are wired to find patterns, even in random events. This tendency (known as apophenia) can lead us to see connections where none exist.

The Misleading Law of Averages

It’s this very tendency that fuels the misconception of the law of averages. We expect randomness to “even out” because we see patterns in short sequences. This can be tempting to believe, especially when dealing with chance events.

Take a coin flip. After five heads in a row, it feels like tails are “due.” But the odds on the next flip are still 50/50. The coin doesn’t remember, and there is no invisible force pushing results back toward balance. That feeling of “due” is your brain’s pattern‑machine misfiring (seeing order where there is none).

The same misfire shows up when you notice your “lucky” number all day, or when you assume a losing streak in markets must soon reverse. The world hasn’t changed; your perception has.

While there are some reasonable mathematical uses of the law of averages, in everyday life, this “law” mostly amounts to wishful thinking (which can lead to dangerous actions).

This natural desire for order and predictability can lead us astray when dealing with chance events.

Why is it Flawed?

The law of averages often leads to a misconception called the gambler’s fallacy. This fallacy is the belief that random events can somehow “correct” themselves to reach an average. In reality, every coin flip, roll of the dice, or spin of the roulette wheel is a fresh start with its own discrete probabilities. The odds remain the same no matter how long the losing streak persists.

It’s also one of the most common fallacies succumbed to by gamblers and traders.

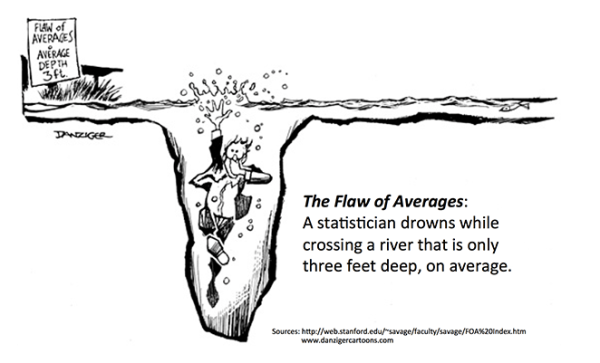

The concept of “Average” is more confusing and potentially damaging than you might suspect.

When the U.S. Air Force designed cockpits around the “average” of 4,000 pilots (average height, average reach, average chest size), almost no real pilot fit the cockpit well. They had designed for a statistical ghost. Only when they re‑engineered for ranges, not averages, did pilots consistently regain control.

Leaders, executives, and investors commit the same error when they build portfolios, forecasts, compensation plans, and product roadmaps around “average” conditions. In reality, performance lives in the extremes — streaks, clusters, and outliers that the average politely hides.

In practice, that looks like:

- Approving a sales plan that “works on average” but can’t survive two bad quarters in a row.

- Pricing a product for the “average customer” and missing the segments that actually drive profit.

- Building a portfolio that’s fine in normal markets but breaks under clustered volatility.

A better approach is to design for ranges — asking “What happens if we get three standard deviations of bad luck?” and “What’s the cost if we’re wrong?” — instead of optimizing for a single point estimate.

It’s a good reminder that ‘facts’ can lie, and assumptions and interpretations are dangerous. It’s why I prefer taking decisive action on something known, rather than taking tentative actions about something guessed.

Below is a video about why we underestimate risk in the face of uncertainty. It discusses the “seven deadly sins” of averages and how a greater understanding of these flaws could prevent future financial meltdowns and other problems.

via ReasonTV

Recognizing Common Misconceptions

It’s important to distinguish the law of averages from the law of large numbers, a well-established statistical principle. The law of large numbers states that as the number of random events increases, the average outcome approaches the expected value. This applies in situations where many trials happen, and while past results of individual events are independent, the law describes the behavior of averages over a large number of trials. For instance, the average weight of a large sample of apples will likely be close to the expected average weight of an apple, even if some individual apples are heavier or lighter than expected. That’s why casinos make money in the long run.

However, in everyday situations (with a limited number of events), the law of averages is generally not a helpful way to think about chance or probabilities. The mistake is smuggling that long‑run logic into short‑run decisions. Your next coin flip, your next quarter, your next product launch is not “owed” anything by the past.

Understanding these misconceptions can help us make better decisions and avoid false expectations based on flawed reasoning.

Psychological Reasons Behind the Belief

Human decision‑making is riddled with biases. As discussed, our pattern‑seeking brains latch onto streaks, and the representativeness heuristic makes us assume that small samples (e.g., last quarter’s returns, last month’s pipeline, a handful of customer anecdotes) must reflect the whole.

Emotional factors also play a role. Our desire for control and fairness encourages comforting stories that “things will even out,” which is why investors double down after a losing streak and leaders assume a bad quarter will automatically be offset by a good one.

Additionally, social influences can reinforce these beliefs. Stories and anecdotes about streaks ending or luck changing often circulate among friends and family, further embedding the misconception into our collective consciousness.

Understanding these psychological reasons helps explain why the law of averages persists despite its flaws. Recognizing these biases can empower us to think more critically about probability and chance events.

Improving Decision-Making in Gambling and Investing

Recognizing the fallacy of the law of averages can significantly enhance decision-making, particularly in gambling and investing. Understanding that each event is independent can help participants make more rational choices. Instead of chasing losses in the hope that a win is “due,” savvy speculators understand that their odds remain constant and may choose to walk away or set strict limits on their betting.

In investing, this knowledge is equally crucial. Many factors influence markets. Nonetheless, believing that a stock “must” rebound after a series of declines too often leads to poor investment decisions. Investors who grasp that past performance does not dictate future results are better equipped to evaluate investments based on fundamentals rather than emotions or flawed expectations.

By dispelling these misconceptions, you can approach gambling or investing with a clearer mindset, reducing the risk of substantial losses driven by erroneous beliefs about probability and chance.

The world will never be as orderly as our brains want it to be. But if you stop designing for the average and start designing for reality, you’ll make fewer avoidable mistakes—and leave less of your future to chance.

You can also eliminate fear, greed, and discretionary mistakes by relying on algorithms to calculate real-time expectancy scores and take the road less stupid. Take a different kind of chance.

Just ask our AI Overlords; they’ll tell you what to expect!

Leave a Reply