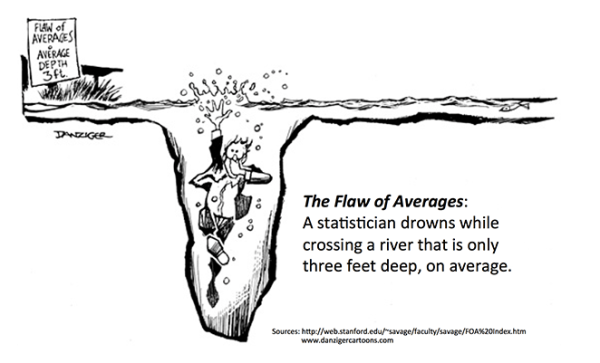

You approve a plan that assumes “average” revenue growth, “average” volatility, and an “average” customer. Then reality shows up: a cluster of bad quarters, a tail‑risk event, a segment that behaves nothing like the model. The problem wasn’t bad luck; it was the flaw of averages — the comforting but dangerous belief that things will naturally “even out” over time.

When you manage money or run a business, trusting that “things will even out” is not a risk-management strategy; it’s a cognitive trap.

This piece is about why the “law of averages” quietly sabotages gamblers, investors, and leaders, and how to design decisions that work in the real world of streaks, outliers, and fat tails.

Our brains are wired to find patterns, even in random events. This tendency (known as apophenia) can lead us to see connections where none exist.

The Misleading Law of Averages

It’s this very tendency that fuels the misconception of the law of averages. We expect randomness to “even out” because we see patterns in short sequences. This can be tempting to believe, especially when dealing with chance events.

Take a coin flip. After five heads in a row, it feels like tails are “due.” But the odds on the next flip are still 50/50. The coin doesn’t remember, and there is no invisible force pushing results back toward balance. That feeling of “due” is your brain’s pattern‑machine misfiring (seeing order where there is none).

The same misfire shows up when you notice your “lucky” number all day, or when you assume a losing streak in markets must soon reverse. The world hasn’t changed; your perception has.

While there are some reasonable mathematical uses of the law of averages, in everyday life, this “law” mostly amounts to wishful thinking (which can lead to dangerous actions).

This natural desire for order and predictability can lead us astray when dealing with chance events.

Why is it Flawed?

The law of averages often leads to a misconception called the gambler’s fallacy. This fallacy is the belief that random events can somehow “correct” themselves to reach an average. In reality, every coin flip, roll of the dice, or spin of the roulette wheel is a fresh start with its own discrete probabilities. The odds remain the same no matter how long the losing streak persists.

Leaders, executives, and investors commit the same error when they build portfolios, forecasts, compensation plans, and product roadmaps around “average” conditions. In reality, performance lives in the extremes — streaks, clusters, and outliers that the average politely hides.

In practice, that looks like:

Approving a sales plan that “works on average” but can’t survive two bad quarters in a row.

Pricing a product for the “average customer” and missing the segments that actually drive profit.

Building a portfolio that’s fine in normal markets but breaks under clustered volatility.

A better approach is to design for ranges — asking “What happens if we get three standard deviations of bad luck?” and “What’s the cost if we’re wrong?” — instead of optimizing for a single point estimate.

It’s a good reminder that ‘facts’ can lie, and assumptions and interpretations are dangerous. It’s why I prefer taking decisive action on something known, rather than taking tentative actions about something guessed.

Below is a video about why we underestimate risk in the face of uncertainty. It discusses the “seven deadly sins” of averages and how a greater understanding of these flaws could prevent future financial meltdowns and other problems.

It’s important to distinguish the law of averages from the law of large numbers, a well-established statistical principle. The law of large numbers states that as the number of random events increases, the average outcome approaches the expected value. This applies in situations where many trials happen, and while past results of individual events are independent, the law describes the behavior of averages over a large number of trials. For instance, the average weight of a large sample of apples will likely be close to the expected average weight of an apple, even if some individual apples are heavier or lighter than expected. That’s why casinos make money in the long run.

However, in everyday situations (with a limited number of events), the law of averages is generally not a helpful way to think about chance or probabilities. The mistake is smuggling that long‑run logic into short‑run decisions. Your next coin flip, your next quarter, your next product launch is not “owed” anything by the past.

Understanding these misconceptions can help us make better decisions and avoid false expectations based on flawed reasoning.

Psychological Reasons Behind the Belief

Human decision‑making is riddled with biases. As discussed, our pattern‑seeking brains latch onto streaks, and the representativeness heuristic makes us assume that small samples (e.g., last quarter’s returns, last month’s pipeline, a handful of customer anecdotes) must reflect the whole.

Emotional factors also play a role. Our desire for control and fairness encourages comforting stories that “things will even out,” which is why investors double down after a losing streak and leaders assume a bad quarter will automatically be offset by a good one.

Additionally, social influences can reinforce these beliefs. Stories and anecdotes about streaks ending or luck changing often circulate among friends and family, further embedding the misconception into our collective consciousness.

Understanding these psychological reasons helps explain why the law of averages persists despite its flaws. Recognizing these biases can empower us to think more critically about probability and chance events.

Improving Decision-Making in Gambling and Investing

Recognizing the fallacy of the law of averages can significantly enhance decision-making, particularly in gambling and investing. Understanding that each event is independent can help participants make more rational choices. Instead of chasing losses in the hope that a win is “due,” savvy speculators understand that their odds remain constant and may choose to walk away or set strict limits on their betting.

In investing, this knowledge is equally crucial. Many factors influence markets. Nonetheless, believing that a stock “must” rebound after a series of declines too often leads to poor investment decisions. Investors who grasp that past performance does not dictate future results are better equipped to evaluate investments based on fundamentals rather than emotions or flawed expectations.

By dispelling these misconceptions, you can approach gambling or investing with a clearer mindset, reducing the risk of substantial losses driven by erroneous beliefs about probability and chance.

The world will never be as orderly as our brains want it to be. But if you stop designing for the average and start designing for reality, you’ll make fewer avoidable mistakes—and leave less of your future to chance.

You can also eliminate fear, greed, and discretionary mistakes by relying on algorithms to calculate real-time expectancy scores and take the road less stupid. Take a different kind of chance.

Just ask our AI Overlords; they’ll tell you what to expect!

It helps to have a map before you’re lost in the woods. It also helps to have one to anticipate the technological challenges, roles, and milestones that will shape your business’s future.

This week, I want to show you how to use ‘desire paths’ and “functional mapping” to build products and platforms that follow the path of least resistance for your customers and your team.

The Road More Traveled …

First, let’s examine a concept in design and transportation called Desire Paths. It refers to the path users take rather than the one intended by the builder.

In business and technology, the same thing happens. Customers, employees, and even markets rarely follow the path you draw on the whiteboard — they follow the path that feels most natural and useful to them. The leaders who notice and design around these ‘desire paths’ create products, processes, and strategies that are easier to adopt and harder to disrupt.

Think about your last internal tool rollout. Did people embrace the official workflow, or did they hack together spreadsheets, Slack messages, and side processes that actually got the work done? Those hacks are desire paths. They reveal where your real product or process needs to go.

Every business knows your product isn’t finished until the users have broken it, found new use cases, and pointed out bugs countless times.

If you are interested, there is an active online community forum that shares examples of Desire Paths. It may give you some ideas and laughs.

I am a creature of habit, and even though much of what I think, feel, or do seems to be happening based on real-time choices or decisions, much of that is just a well-worn rut of unconscious behavior.

As a subtle reminder to my son, who recently got married, I told him to expect many of his existing desire paths to change (even if he doesn’t want them to). The same is true for your company: big changes in context overwrite old paths, no matter how comfortable they feel. The question is whether you notice the new paths and design around them — or cling to the old map.

The lesson … It’s often easier to account for or take advantage of human nature (or nature) than to fight against it.

Building A Better Roadmap …

Here is a short video on how this relates to your business and tech adoption. I call it Functional Mapping. Check it out.

The video provides additional depth and detail beyond what’s covered in this post. I encourage you to watch it for a more complete perspective.

Functional Mapping is a way to visualize who does what, when, and why throughout the journey from thought to thing. It forces you to match roles and personalities to the specific phase of the journey.

Understanding the natural paths of technological development and human nature makes it easier to anticipate the capabilities, constraints, and milestones that likely will define your path forward.

That means understanding the different types of users and what they expect to do or accomplish.

Below is a diagram we use at Capitalogix to help us anticipate the roles (including their personality, tendencies, and skills) needed to navigate the milestones along our journey. For example, the person who imagines a product often loves ambiguity and possibility, while the person who builds it prefers precision and proof. And that knowledge helps you choose the person for the role, as well as the materials and resources you provide them with.

If you treat them as interchangeable, you create friction. If you map their functions clearly, you create flow.

While it’s easy to pay attention to what changes often, it’s also important to understand what doesn’t change. As long as people are building things for people, it’s crucial to recognize that both creation and adoption are heavily influenced by human nature (which isn’t likely to change).

Understanding this helps you anticipate and navigate the strengths, weaknesses, opportunities, and threats you will likely find on your path.

You’ve probably heard me talk about how Capabilities become Prototypes. Then, Prototypes become Products. And, ultimately, Products become Platforms.

Here is a simple example. Let’s describe a new AI model as a capability. When you wrap it into a simple internal tool, it becomes a prototype. Once it consistently solves a valuable problem for someone, you can turn it into a product they can buy. If that product becomes central to how customers run their business, it evolves into a platform that other products and services plug into.

The point is that the model is fractal. That means it works on many levels of magnification or iteration.

What first looks like a product is later seen as a prototype for something bigger.

SpaceX’s goal to get to Mars feels like their North Star right now … but once it’s achieved, it becomes the foundation for new goals.

This Framework helps you validate capabilities before sinking resources into them.

It helps you anticipate which potential outcomes you want to accelerate. It really means beginning with the end in mind. So, rather than simply figuring out the easiest next step, you have to figure out which path is most likely to lead to your desired outcome.

Pick one area of your business where people already ignore the ‘paved path’ and follow their own route. This week, map that desire path, identify which capability it represents, and ask what it would take to turn it into a prototype or product instead of fighting it.

The world is changing fast! Hope you’re riding the wave instead of getting caught in the riptide!

In 2016, I received this e-mail from my oldest son.

Date: Saturday, October 22, 2016 at 7:09 PM Subject: FYI: Security Stuff

FYI – I just got an alert that my email address and my Gmail password were available to be purchased online.

I only use that password for my email, and I have 2-factor enabled, so I’m fine. Though this is further proof that just about everything is hacked and available online.

If you don’t have two-factor enabled on your accounts, you really need to do it.

Since then, security has only become a bigger issue. I wrote about the Equifax event, but there are countless examples of similar events (and yes, I mean countless).

When people think of hacking, they often think of a Distributed Denial of Service (DDOS) attack or the media representation of people breaking into your system in a heist.

In reality, the greatest weakness is people; it’s you … the user. It’s the user who turns off automatic patch updating. It’s the user who uses thumb drives. It’s the user who reuses the same passwords. It’s the user who falls for social engineering. Each of those choices may seem like a mistake, but they also represent some hacker’s favorite pattern to exploit.

Whether it’s malicious or unintentional, humans are often the biggest security weakness.

It’s impossible to protect yourself completely, but there are many simple things you can likely do better.

Use better passwords … Even better, don’t know them. You can’t disclose what you don’t know. Instead, use a password manager like LastPass or 1Password, which can also suggest complex passwords for you.

Check if any of your information has been stolen via a website like HaveIBeenPwned or F-Secure.

Keep all of your software up to date (to avoid extra vulnerabilities).

Don’t use public Wi-Fi if you can help it (and use a trustworthy VPN if you can’t).

Don’t put information into GPTs that you want to keep private.

Have a firewall on your computer and a backup of all your important data.

Never share your personal information on an e-mail or a call that you did not initiate – if they legitimately need your information, you can call them back.

Don’t trust strangers on the internet (no, a Nigerian Prince does not want to send you money).

How many cybersecurity measures you take comes down to two simple questions … First, how much pain and hassle are you willing to deal with to protect your data? And second, how much pain is a hacker willing to go through to get to your data?

It doesn’t make sense to put all your data in a lockbox computer that never connects to a network … Nevertheless, it might be worth going to that extreme for some of your data.

Think about what the data is worth to you, or someone else, and protect it accordingly.

My son reminds, “You’ve already been hacked … the important question is whether you’ve been targeted?” Something to think about!

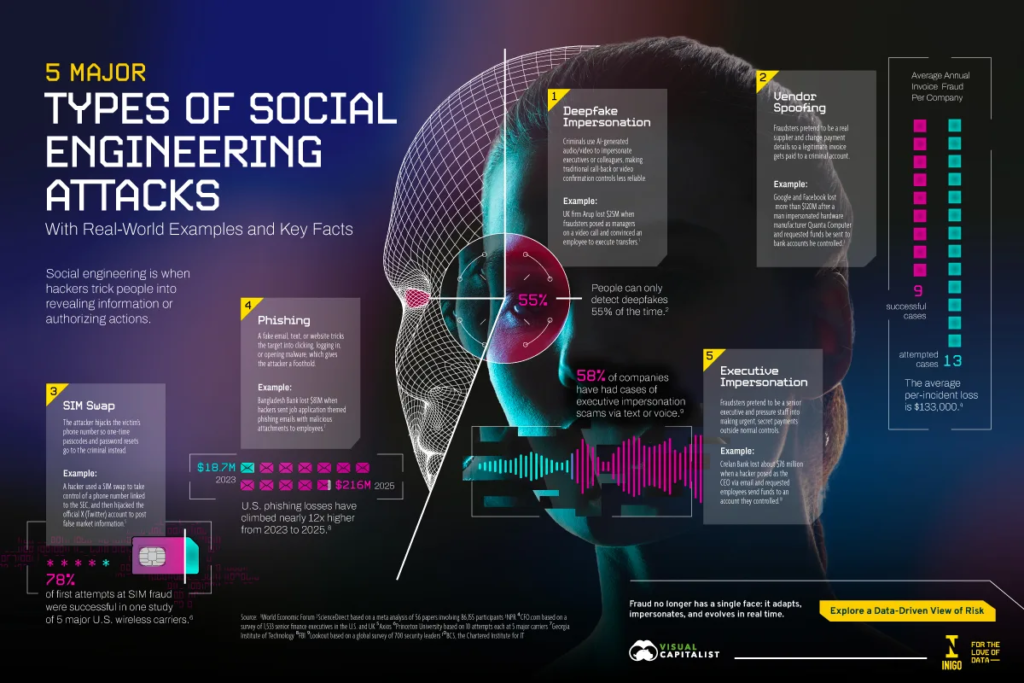

For most of human history, scams were relatively simple. A stranger sold fake miracle cures from the back of a wagon. A con artist ran a shell game on a busy street corner. Someone forged signatures, counterfeited checks, or promised riches through a too-good-to-be-true investment scheme. The tools changed with each era, but the mechanics stayed familiar: gain trust, create urgency, exploit emotion.

The internet accelerated everything.

In the early days online, scams were often obvious and almost amateurish. Chain emails promised bad luck if you didn’t forward them to ten friends. Pop-ups claimed you had “won” a valuable prize. People in chatrooms pretended to be tech support employees asking for passwords, while others sold fake concert tickets or nonexistent items through forums and classifieds. On platforms like AOL, MSN Messenger, IRC, and early online marketplaces, anonymity created an entirely new playground for deception. Most scams were still relatively small-scale, relying on volume and the assumption that someone would eventually fall for them.

Today, fraud operates at an entirely different level.

Modern scams can involve organized criminal networks, rogue nation-states, stolen datasets, spoofed phone numbers, AI-generated voices, cloned websites, and highly targeted psychological profiling. A scammer might know where you work, who your bank is, what school your child attends, and which recent purchase is waiting on your doorstep. What once looked like a poorly written e-mail from a foreign prince can now look indistinguishable from a legitimate message from your employer, your bank, or even a family member.

Yet despite all the technological sophistication, the core principle has barely changed. Social engineering still depends on manipulating human behavior: fear, urgency, trust, greed, loneliness, authority, or curiosity. The software has evolved. Human psychology hasn’t.

The common thread across all of these attacks is that they exploit people more than technology. Fraudsters are increasingly bypassing traditional cybersecurity defenses not by breaking systems, but by manipulating trust, authority, urgency, and routine behavior. As AI lowers the cost of impersonation and allows scams to scale globally, social engineering is becoming one of the defining fraud risks of the digital era.

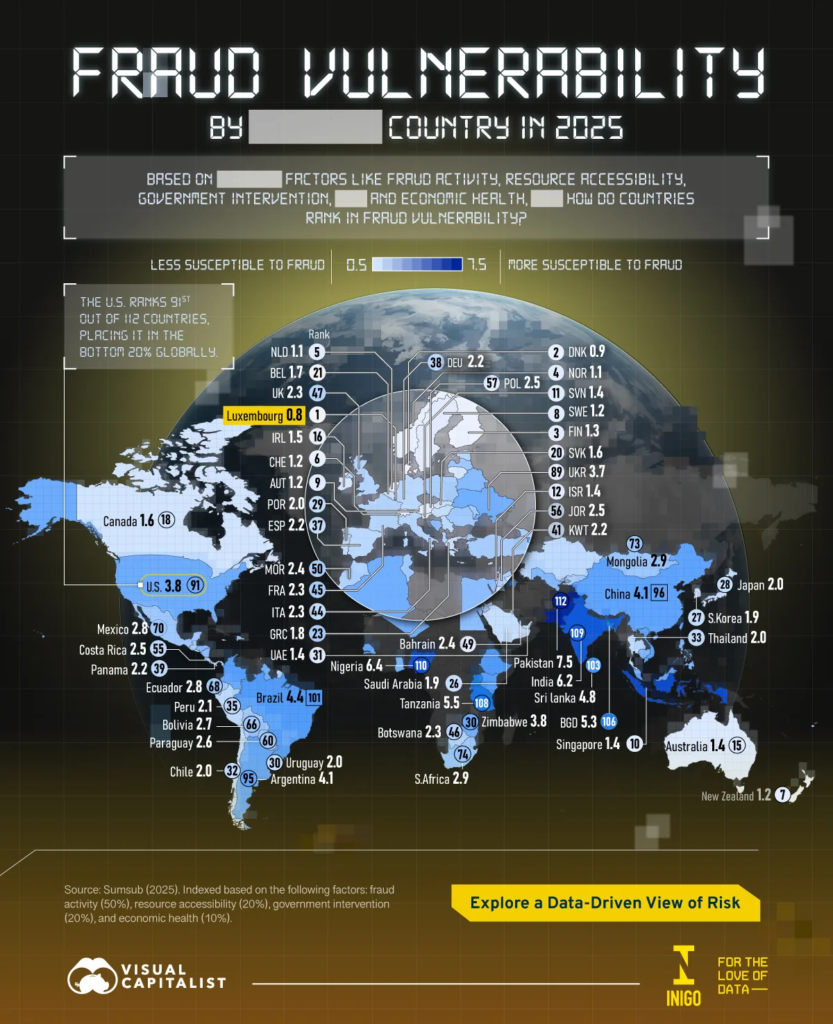

Sumsub developed the index based on four main factors: fraud activity, resource accessibility, government intervention, and economic health. Lower scores suggest better resilience against fraud, whereas higher scores indicate increased risk exposure.

Many lower-ranked countries face challenges such as weaker enforcement systems, limited digital protections, and economic instability. These conditions increase the likelihood of fraudulent activities proliferating.

But fraud isn’t only an issue in emerging countries.

America ranked 91st, putting us in the bottom 20% globally.

We’ve been preaching about cybersecurity for years, and as always, the greatest risk is the human-in-the-loop.

The difference now is that AI is making it cheaper and easier than ever to target that human at scale.

You may not have fallen for a scam yet … but I bet you’ve fallen for an AI video. Regardless, the odds that your team, your vendors, or your portfolio companies will be tested are rising fast.

Make sure you have protections and fail-safes at both the company and personal levels.

In the age of AI, we’re obsessed with better answers. But the real leverage may come from better questions.

It’s easier to solve someone else’s problem than your own. Why? Because your biases, emotions, and problem-solving frameworks become part of the problem. Likewise, your blind spots likely go unexamined when you’re both the observer and the subject.

As an entrepreneur, I strive to be objective about the decisions I make. Towards that goal, using key performance indicators, getting different perspectives from trusted advisors, and relying on tried-and-true decision frameworks all help.

Mindfulness as a Decision Framework

Combining all three creates a form of “mindfulness” that comes from dispassionately observing from a perspective of all perspectives.

That almost-indifferent, objective approach is also where exponential technologies like AI excel. They amplify intelligence by helping make better decisions, take smarter actions, and continually improve performance.

When I shot this video, AI was still relatively limited.

In just a few years, the technology has come so far. When I originally published the video, I suggested that:

The future of AI will likely be based on swarm intelligence, where many specialist components communicate, coordinate, and collaborate to view a situation more objectively, better evaluate the possibilities, and determine the best outcome in a dynamic and adaptable way that adds a layer of objectivity and nuance to decision-making.

Five years later, that prediction has largely materialized. Multi-agent frameworks, retrieval-augmented generation, and tool-using LLMs now orchestrate specialized components to tackle complex problems. The architecture isn’t identical to biological swarm intelligence, but the principle holds: better decisions emerge from coordinated, specialized perspectives, and from understanding the actual purpose of your tools.

What Hasn’t Changed

AI is a powerful solution for a seemingly infinite number of problems. But, much like the internet, it’s easy to get distracted by shiny objects, flashy intrusions, or compelling answers.

It is important to stay mindful and diligent as you apply AI and AI agents to your business.

Many of my friends are getting excited about these tools, and they’re using them for countless capabilities, but they’re not necessarily doing a good job of evaluating whether they should be.

Sometimes, you shouldn’t even be looking for the right answer, you should be looking for the right question.

The Importance of Better Questions

One of the lessons I teach to our younger employees is that an answer is not THE answer. It’s intellectually lazy to think you’re done simply because you come up with a solution. There are often many ways to solve a problem, and the goal is to determine which yields the best results.

Even if you find THE answer, it is likely only THE answer temporarily. It is a step in the right direction that buys you time to learn, improve, and re-evaluate.

Mindfulness comes from slowing down, stepping back, and looking at something from multiple perspectives, and AI can be a powerful tool for that when used intentionally. It can help us explore different viewpoints, challenge assumptions, and think more broadly.

But the greatest benefit of AI may not be in generating better answers. More often, it comes from helping us ask better questions.

Used mindfully, AI becomes less of a shortcut to conclusions and more of a tool for deeper thinking.

Recently, I’ve started using AI to sharpen my questions, and it’s changing the way I approach problems. At first, that sounds abstract, but in practice it forces a very different kind of thinking. Instead of immediately searching for conclusions, you start asking what actually makes a question “better” in the first place. How do you move from a vague sense of uncertainty to a question precise enough to reveal something useful?

When I’m evaluating a project now, I rarely ask AI something broad like, “Is this a good opportunity?” Questions like that usually produce predictable answers. Instead, I use AI to pressure-test my own thinking. I’ll ask it to identify the assumptions underneath the idea, explore what would have to be true for the project to fail, or point out the questions I haven’t considered yet. The process feels less like outsourcing thought and more like refining it.

That shift — from answer-seeking to question-sharpening — has changed how I handle ambiguity and make decisions. It has also changed what I consider trustworthy. I’ve started building what I think of as a “question pattern library”: prompts and frameworks that consistently help add structure to messy situations. Some questions help clarify the framing by forcing you to define the real decision being made rather than reacting to surface-level symptoms. Others establish criteria, helping determine how success should actually be measured before debating solutions. And some are designed to expose bottlenecks by identifying which assumption, if proven false, would completely change the next step.

Over time, I’ve realized these questions work best when they build on each other. At important checkpoints, I’ll often run through a simple sequence: What became clearer? What does this change? Why does it matter? What’s the next best move? The answers themselves matter less than the way the questions force clearer thinking.

The more I use AI this way, the more I think its greatest value may not be generating better answers at all. Used mindfully, its real strength is helping us examine our own thinking more carefully. Better questions create better distinctions, and better distinctions usually lead to better judgment. So before asking AI for an answer this week, it may be worth asking it to help you frame a better question first. You might discover that the most valuable part of the interaction isn’t the response, but the thinking process that led to it.

So whether you are a glass-half-full or a glass-half-empty person, you have plenty of ammunition.

The news cycle is designed to monetize fear, so it reliably amplifies what is fragile, broken, or uncertain. But if you shift focus from the headlines to the data, the global economy in 2026 looks far more resilient (and more opportunity-rich) than most people realize.

In this week’s commentary, I’ll walk through a few key charts that cut through the noise and highlight where growth, risk, and leverage are actually shifting.

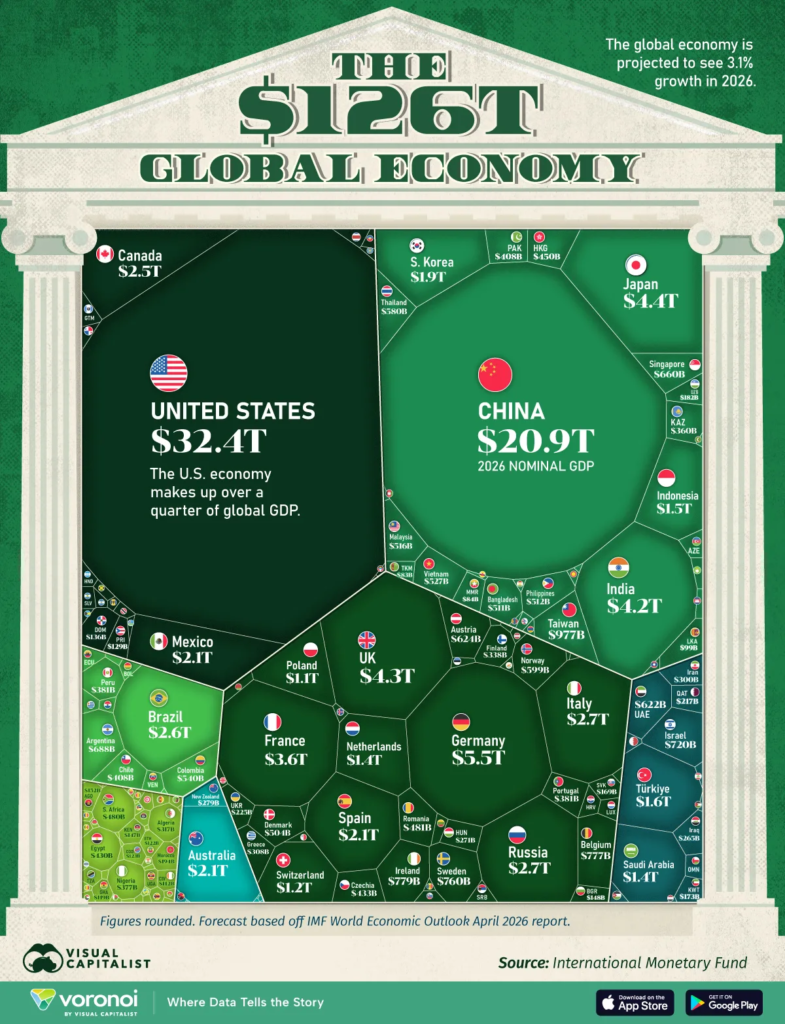

The world economy is slated to reach $126 trillion this year, with four countries accounting for over half of that. Who tops the list?

The United States. As we have for over 100 years.

The graphic below visualizes the global economy as a whole using IMF projections from the April 2026 World Economic Outlook, breaking down nearly 200 countries by their share of nominal GDP.

Infographic showing just four countries generate roughly half of all economic activity worldwide.

Just four countries generate roughly half of all economic activity worldwide (U.S. ~$32T, China ~$21T, Germany ~$5T, and Japan ~$4T ). That concentration of economic power is striking, but as we’ll see, size alone doesn’t tell you who’s winning the next decade.

Size Doesn’t Equal Speed

Among the four largest economies, China is expected to lead with a projected 4.4% real growth in 2026, while the U.S. is anticipated to grow a solid 2.3%. In contrast, Germany and Japan (which have experienced years of stagnation) are forecast to grow only around 0.7–0.8%.

China’s strong performance continues a trend observed over the past several decades, despite facing challenges such as a demographic slowdown and an ongoing property sector crisis.

Once you look past the largest economies, there are real opportunities in large, fast‑growing markets across Asia. For example, India, at roughly $4.2 trillion in GDP, and Indonesia, at $1.5 trillion, are on track to play a much bigger role in the global order.

With a forecasted 6.6% growth rate in 2026, India could surpass the United Kingdom and potentially Japan by 2028 — driven by a demographic dividend, expanding services exports, and rapidly maturing digital infrastructure. For entrepreneurs and investors, that shift isn’t just trivia; it should inform where you place bets, partner, and build.

Tariffs, Trade, and the Debt Behind It All

Since early 2025, high-tariff policies implemented by the U.S. have caused downward revisions in growth forecasts for several economies, especially in North America.

Canada and Mexico are especially exposed. With U.S.-Canada relations strained and negotiations over a trilateral trade agreement progressing slowly, the North American economic bloc faces increasing uncertainty.

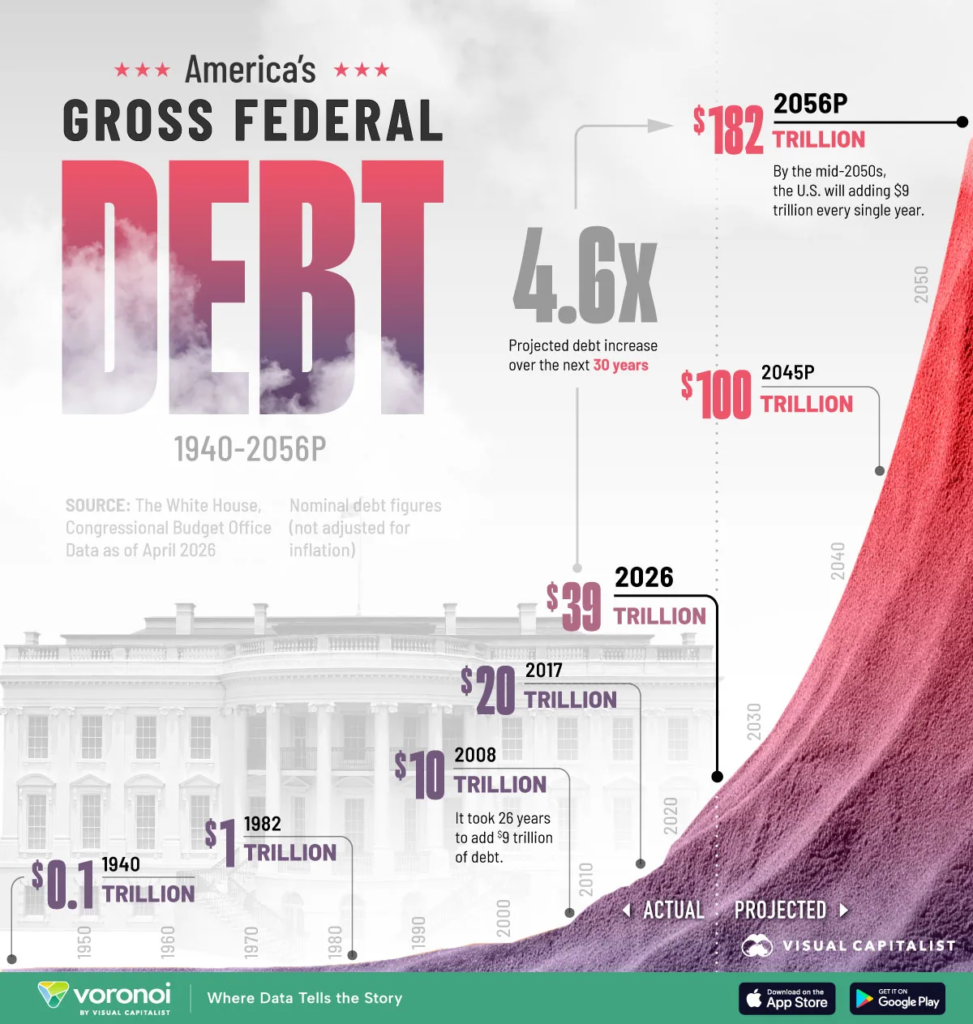

After World War II, it took over 60 years for U.S. debt to reach $10 trillion. The next $10 trillion took 9 years to reach following the 2008 financial crisis. In the 2020s, pandemic spending compressed the interval to just five years.

By the 2050s, each additional $10 trillion could take just one to two years.

That is under modest assumptions, with no new wars, no recessions, and manageable interest rates. Even so, debt projections still reach $182 trillion by 2056. For context, we’re at about $39 Trillion now.

The real story of the global economy isn’t just told with GDP rankings. While America and China dominate those numbers, it’s clear the landscape is changing.

Traditional economic metrics might become less relevant in a world where regional conflicts, supply chain dynamics, and technological innovation can reshape global power dynamics overnight.

In the longer term, birth rates and the growth of middle-class infrastructure are strong predictors of what lies ahead. That’s part of why we see so much growth in India and Indonesia.

GDP alone doesn’t measure what truly matters in the modern global economy.

The Variable That Changes Everything

Looking beyond traditional economic metrics, I believe artificial intelligence will emerge as one of the most critical factors driving power, progress, and wealth creation in the coming years. It’s likely to become both the most coveted resource and the capability we’ll most actively seek to deny our adversaries.

Economies that combine large markets, strong digital infrastructure, and responsive regulatory environments will be positioned to capture outsized gains. Those that lag on talent, compute, or data governance may see their nominal GDP grow while their strategic leverage erodes.

Obviously, AI is something I think about and write about in many other articles, so even though I won’t add a detailed section here, it’s worth noting that AI is going to change the relative weight and importance of many other things in increasingly exponential ways.

In conclusion, the scoreboard is changing on three fronts at once: where growth lives, how policy shapes risk, and how AI alters productivity and power. If you’re allocating capital or building companies in this environment, the advantage goes to leaders who can see beyond the fear‑driven headlines to where the real leverage is emerging.