We live in interesting times!

So whether you are a glass-half-full or a glass-half-empty person, you have plenty of ammunition.

The news cycle is designed to monetize fear, so it reliably amplifies what is fragile, broken, or uncertain. But if you shift focus from the headlines to the data, the global economy in 2026 looks far more resilient (and more opportunity-rich) than most people realize.

In this week’s commentary, I’ll walk through a few key charts that cut through the noise and highlight where growth, risk, and leverage are actually shifting.

For example, you can focus on the $100 trillion global debt … but you could also focus on how U.S. states’ GDPs compare to global GDPs.

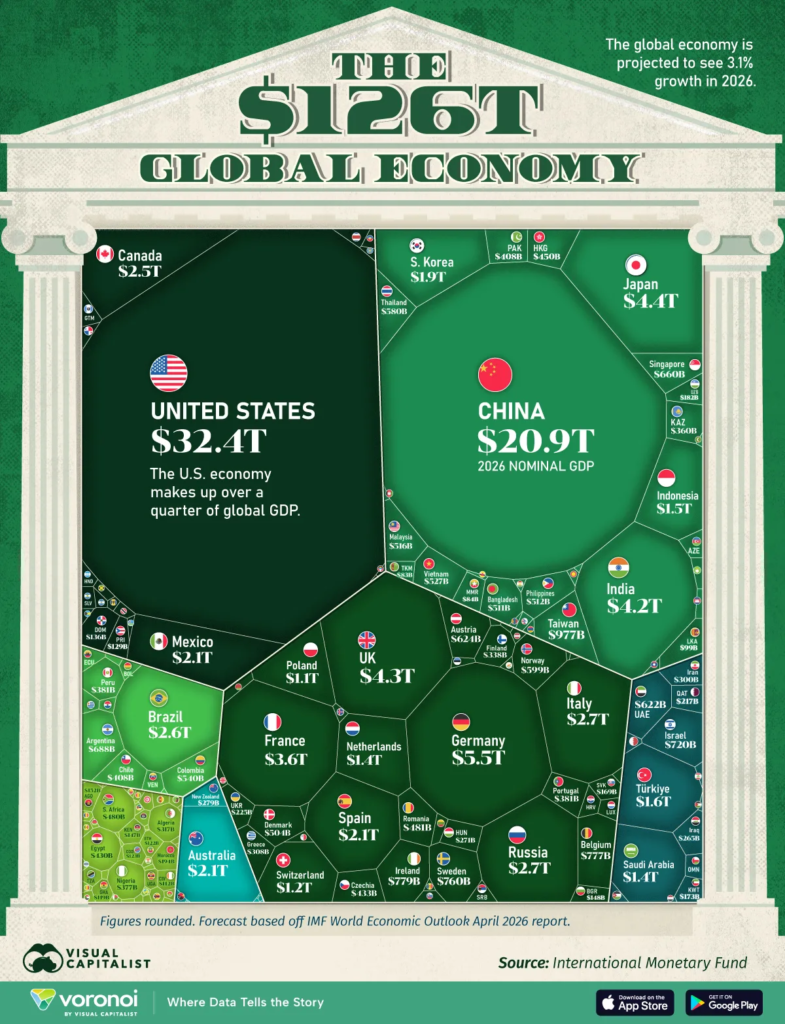

The $126 Trillion Scoreboard

The world economy is slated to reach $126 trillion this year, with four countries accounting for over half of that. Who tops the list?

The United States. As we have for over 100 years.

The graphic below visualizes the global economy as a whole using IMF projections from the April 2026 World Economic Outlook, breaking down nearly 200 countries by their share of nominal GDP.

via visualcapitalist

Just four countries generate roughly half of all economic activity worldwide (U.S. ~$32T, China ~$21T, Germany ~$5T, and Japan ~$4T ). That concentration of economic power is striking, but as we’ll see, size alone doesn’t tell you who’s winning the next decade.

Size Doesn’t Equal Speed

Among the four largest economies, China is expected to lead with a projected 4.4% real growth in 2026, while the U.S. is anticipated to grow a solid 2.3%. In contrast, Germany and Japan (which have experienced years of stagnation) are forecast to grow only around 0.7–0.8%.

China’s strong performance continues a trend observed over the past several decades, despite facing challenges such as a demographic slowdown and an ongoing property sector crisis.

Once you look past the largest economies, there are real opportunities in large, fast‑growing markets across Asia. For example, India, at roughly $4.2 trillion in GDP, and Indonesia, at $1.5 trillion, are on track to play a much bigger role in the global order.

With a forecasted 6.6% growth rate in 2026, India could surpass the United Kingdom and potentially Japan by 2028 — driven by a demographic dividend, expanding services exports, and rapidly maturing digital infrastructure. For entrepreneurs and investors, that shift isn’t just trivia; it should inform where you place bets, partner, and build.

Tariffs, Trade, and the Debt Behind It All

Since early 2025, high-tariff policies implemented by the U.S. have caused downward revisions in growth forecasts for several economies, especially in North America.

Canada and Mexico are especially exposed. With U.S.-Canada relations strained and negotiations over a trilateral trade agreement progressing slowly, the North American economic bloc faces increasing uncertainty.

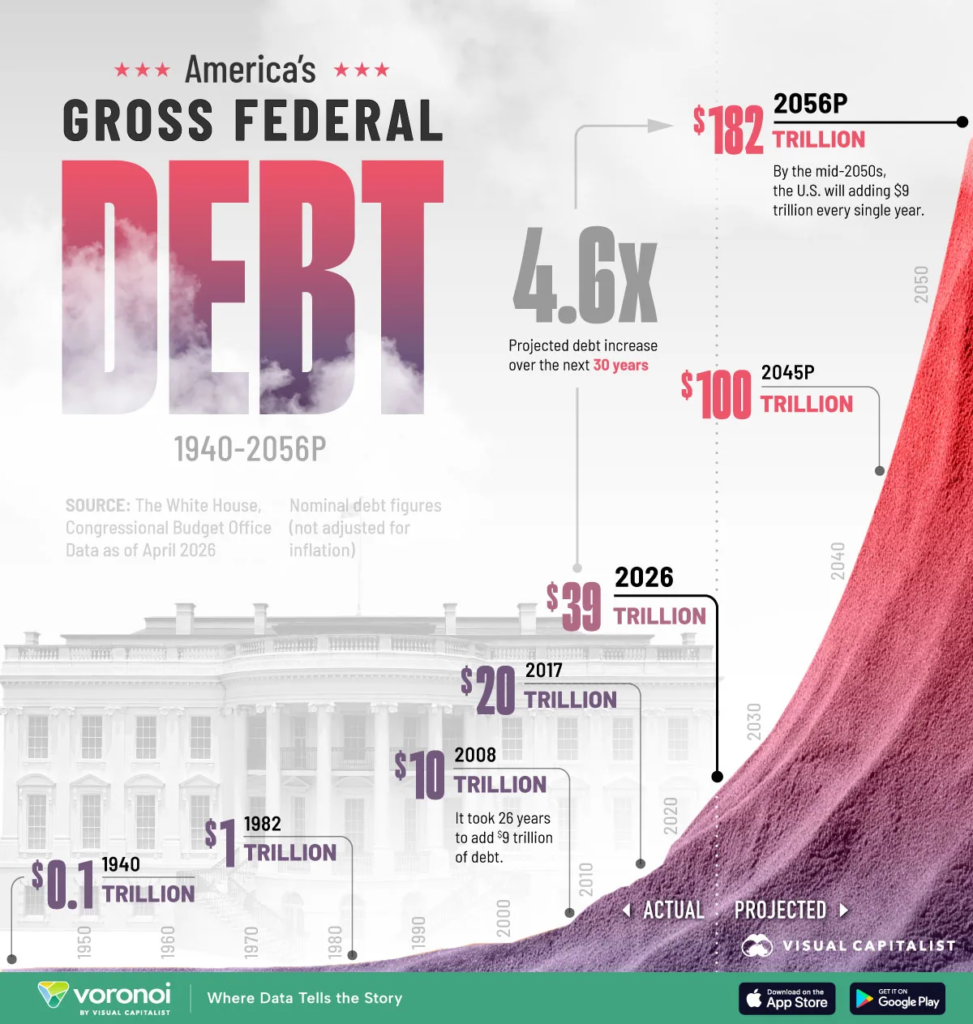

via visualcapitalist

After World War II, it took over 60 years for U.S. debt to reach $10 trillion. The next $10 trillion took 9 years to reach following the 2008 financial crisis. In the 2020s, pandemic spending compressed the interval to just five years.

By the 2050s, each additional $10 trillion could take just one to two years.

That is under modest assumptions, with no new wars, no recessions, and manageable interest rates. Even so, debt projections still reach $182 trillion by 2056. For context, we’re at about $39 Trillion now.

That data comes from the Congressional Budget Office (CBO) and the White House as of March 2026.

So is the Glass Half Full or Half Empty?

The real story of the global economy isn’t just told with GDP rankings. While America and China dominate those numbers, it’s clear the landscape is changing.

Traditional economic metrics might become less relevant in a world where regional conflicts, supply chain dynamics, and technological innovation can reshape global power dynamics overnight.

In the longer term, birth rates and the growth of middle-class infrastructure are strong predictors of what lies ahead. That’s part of why we see so much growth in India and Indonesia.

GDP alone doesn’t measure what truly matters in the modern global economy.

The Variable That Changes Everything

Looking beyond traditional economic metrics, I believe artificial intelligence will emerge as one of the most critical factors driving power, progress, and wealth creation in the coming years. It’s likely to become both the most coveted resource and the capability we’ll most actively seek to deny our adversaries.

Economies that combine large markets, strong digital infrastructure, and responsive regulatory environments will be positioned to capture outsized gains. Those that lag on talent, compute, or data governance may see their nominal GDP grow while their strategic leverage erodes.

Obviously, AI is something I think about and write about in many other articles, so even though I won’t add a detailed section here, it’s worth noting that AI is going to change the relative weight and importance of many other things in increasingly exponential ways.

In conclusion, the scoreboard is changing on three fronts at once: where growth lives, how policy shapes risk, and how AI alters productivity and power. If you’re allocating capital or building companies in this environment, the advantage goes to leaders who can see beyond the fear‑driven headlines to where the real leverage is emerging.

Onwards!